Launch Your Mission Faster with Fiscal Sponsorship

Skip years of nonprofit paperwork. Embolden WI gives your initiative 501c3 status, administrative backbone and over 20 years of nonprofit management and advocacy - so you can focus on impact from day one.

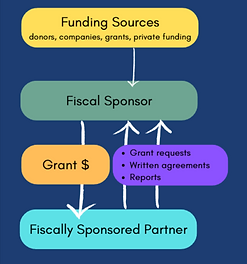

What is fiscal sponsorship?

A fiscal sponsor extends its tax-exempt 501(c)(3) status to your project — letting you accept tax-deductible donations and apply for grants without spending years building your own nonprofit infrastructure.

Embolden WI's comprehensive model goes further: we handle the legal, financial, and compliance overhead so your leaders can focus entirely on advancing health equity, health justice, and civic health in Wisconsin.

Months, not years

Months, not years

Get up and running with full nonprofit status right away

20+ years

20+ years

of Embolden's WI financial history back your grant applications

Flat cost-sharing

Predictable costs well below typical nonprofit overhead

Why Partner with Embolden WI?

Embolden WI supports Wisconsin-based projects focused on health equity, health justice, and civic health. As a fiscal sponsor, we let you operate under an existing 501(c)(3), raise funds, and focus on your work—without the administrative burden of starting from scratch. It’s often a faster, lower-risk way to launch and see what your idea can become.

Here are just 3 reasons why you should consider partnering with Embolden WI as your fiscal sponsor:

1

You Can Focus on Impact, Not Infrastructure

Embolden WI absorbs the legal, financial, and compliance burden so your team can spend every hour advancing your mission.

2

You Gain Immediate Credibility & Access to Funding

Accept tax-deductible donations and pursue grant funding from day one — without waiting years for 501(c)(3) status.

3

It's a Smart, Flexible Plan for Growth

Stay with us as a permanent home or spin off into your own nonprofit when you're ready. Either way, we reduce your risk.

Two sponsorship models

Model A - Comprehensive fiscal sponsorship

Best for projects just getting started, short-term initiatives, or organizations feeling the weight of growing administrative costs. Your initiative operates under Embolden WI's umbrella — our financial history becomes your financial history, giving funders confidence their money is in good hands.

-

Full administrative support included

-

Controlled, predictable costs

-

Leverage our 20-year grant history

-

Option to spin off into your own nonprofit later

Model C - Pre-approved grant sponsorship

You already have a funding source in mind but need 501(c)(3) status to apply. Your project stays its own legal entity — but gains access to funding sources that would otherwise be out of reach. Embolden WI handles the board oversight and audits required to qualify for tax-deductible funds.

-

Project keeps its own legal identity

-

Unlocks grant and donation sources

-

No need for your own board or audits

Common questions

Ready to find out if fiscal sponsorship is right for you?

Two simple steps to get started - no commitment required

Fiscal Sponsorship Resources

-

Fiscal Sponsorship: A balanced overview (Nonprofit Quarterly)

-

Alternatives to starting a nonprofit (Minnesota Council of Nonprofits)

-

Fiscal Sponsor versus Fiscal Agency (CharityLaw Blog)

-

Fiscal Sponsorship: a 360 Degree Perspective, Trust for Conservation Innovation.

-

Fiscal Sponsorships: Get the benefits of a charity without being one (Chartiable Allies)

-

Fiscal Sponsorship: A 360 Degree Perspective (Trust for Conservation Innovation)